On 12 July 2023, the Foreign Subsidies Regulation (FSR) came into force. Since 12 October 2023, the notification obligation for concentrations and public procurement above certain thresholds applies. The FSR needs to be considered whenever subsidies are awarded to businesses that will operate in the EU single market.

Overview of the Foreign Subsidies Regulation

Subsidies granted by EU member states are subject to scrutiny under EU state aid rules and subsidies granted in the UK are subject to scrutiny under the Subsidy Control Act 2022 – prior to the FSR, subsidies granted by non-EU governments went unchecked. The FSR rules enable the European Commission to tackle foreign subsidies that cause distortions and undermine the level playing field for companies operating in the internal market, while remaining open to trade and investment.

Under the FSR, the concept of a foreign subsidy is deemed to exist where “a third country provides, directly or indirectly, a financial contribution which confers a benefit on an undertaking engaging in an economic activity in the internal market and which is limited, in law or in fact, to one or more undertakings or industries”.1 Financial contributions may include a transfer of funds or liabilities, the foregoing of revenue that is otherwise due, or the provision or purchase of goods or services. A foreign subsidy is distortive if it “is liable to improve the competitive position of an undertaking in the internal market [and] … actually or potentially negatively affects competition in the internal market.”2

Additional powers to investigate

The FSR gives the European Commission additional powers by allowing it to investigate businesses that have received financial assistance outside of the scope of EU state aid law which have the potential to distort the EU single market.

The FSR introduces three procedures:

- "A notification-based procedure to investigate concentrations involving financial contributions granted by non-EU governments, where the acquired company, or one of the merging parties or the joint venture generates an EU turnover of at least EUR 500 million and the parties were granted foreign financial contributions of more than EUR 50 million in the last three years"

- "A notification-based procedure to investigate bids in public procurement procedures, involving financial contributions by non-EU governments, where the estimated contract value is at least EUR 250 million and the bid involves a foreign financial contribution of at least EUR 4 million per third country in the last three years"

- "An ex officio procedure to investigate all other market situations, where the European Commission can start a review on its own initiative"

Above the relevant thresholds, the parties are required to notify financial contributions received from non-EU public authorities prior to concluding a concentration or to a public procurement award. If the European Commission suspects the existence of distortive foreign subsidies, it has powers to request ad-hoc notifications for concentrations and public procurement procedures below the thresholds. While the Commission's review is underway, the concentration can't be completed and the investigated bidder can't be awarded the contract.

Redressive measures

The Commission has the power to levy fines of up to 10% of the aggregate turnover of a business in the preceding financial year if a notification isn't made prior to the implementation of a measure. Where a distortive subsidy is identified, then the FSR gives the Commission discretion as to the redressive measures it chooses to implement to remedy the distortion in the internal market, unless it has accepted commitments offered by that undertaking.

Such measures could include fair, reasonable, and non-discriminatory conditions to infrastructure (FRAND), reducing capacity or market presence, refraining from certain investments, divestment of certain assets, requiring a recipient to adapt its governance structure, or repayment of the foreign subsidy including an appropriate interest rate.

Implications and scope

It's possible for a business to benefit from significant subsidies awarded outside the scope of EU state aid law and to subsequently trade, at an advantage, within the EU single market. The objective of the FSR is to close this gap by addressing the impact of such subsidies at the point they are considered to distort the single market.

The regulation is likely to mean burdensome compliance and increases transaction risk, particularly for multinationals or entities with complex delivery structures and supply chains with a significant European nexus. EU undertakings active in non-EU countries that are granted foreign financial contributions are also within the scope of the FSR.

If EU firms, or those with a substantial EU arm (a UK firm operating in the EU, for example) accept financial assistance from non-EU governments, they'll want to reassure themselves that the assistance being provided isn’t considered a subsidy. This assessment is likely to hinge on the Market Economy Operator Principle (MEOP), or the Commercial Market Operator (CMO) principle, as it's referred to in the UK Subsidy Control Act 2022. This assesses whether, in similar circumstances, a private investor of a comparable size operating in normal market economy conditions would have made the same investment.

Bespoke competition analysis for complex issues

Learn more about how our Competition economics services can help you

MEOP/CMO test

To test whether the funding confers an economic advantage, the proposed transaction should be evaluated against what is (or is believed could be) undertaken by a private sector ‘commercial’ entity.

The MEOP test is commonly used to determine that the proposed support is being granted on a commercial basis and therefore doesn't confer an economic advantage that's not available on market terms. The MEOP test is typically applied on a forward-looking basis to assess whether an economic transaction is in line with market conditions, ie, whether the public authority’s actions are in line with those of a market economy operator. The decisive element is whether the public bodies acted as a market economy operator would have done in a similar situation.

For the purposes of this test, it's only a public authority’s commercial objectives that are relevant for the assessment. Any public policy objectives, such as wider economic or social impacts, shouldn't be included when assessing whether the financial assistance in question confers an economic advantage.

A private operator can include vendors, investors, and creditors. The relevant operator will depend upon on the type of financial assistance that the public authority is providing, which may include loans, direct funds or purchases of goods and services. For example, a loan provided by a public authority won't be considered to confer an economic advantage to an enterprise if the loan might be provided by a private sector bank or private sector shareholders on the same terms.

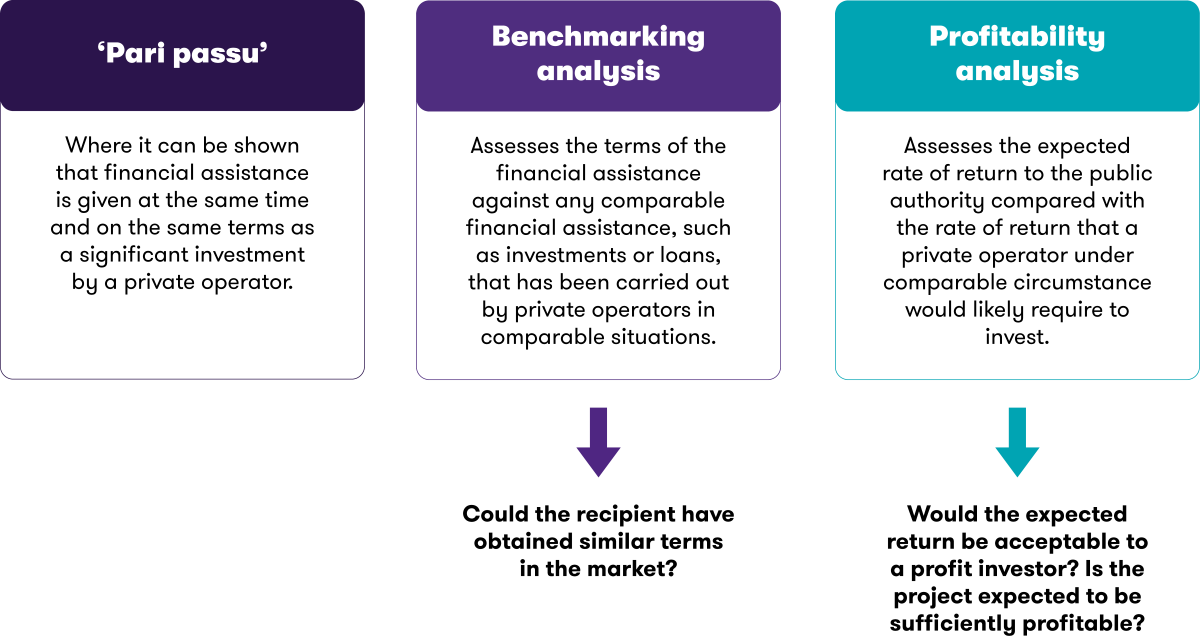

Versions of the CMO test – examples

![Versions of the CMO test – examples]()

There are a variety approaches that may be considered to establish compliance with market conditions. The approach should be tailed to the context and specifics of the assessment, as described in the examples below.

How public authorities can show compliance with the CMO principle – examples

![How public authorities can show compliance with the CMO principle – examples]()

Where a foreign subsidy is identified

If the financial assistance is deemed to be a subsidy, it'll be necessary to consider the impacts of the funding on international trade and investment. This will require detailed analysis of the relevant markets. For instance, this may include assessment of the entity’s EU operations, size of the enterprise and market presence, upstream and downstream supply chains, beneficiaries, the extent to which the economic benefit is passed-on, and materiality of the potential effects.

The more complicated the activities and corporate structure of an enterprise, the more complex this economic assessment is likely to be.

Enterprises with a significant EU presence may consider methods such as transfer pricing, separate accounting, separation of entities or a combination of these methods to ensure that a subsidy granted by a non-EU government doesn't indirectly benefit activities in the EU.

Support with FRS compliance

Our economic consulting team can support you with the identification of subsidies, deal structure and implications, MEOP/CMO analysis (using benchmarking and other assessment methods), counterfactual assessment, subsidy principles assessment, analysis of effects on competition, trade, and investment, and market distortion assessments.

For insight and guidance, get in touch with Hana Hammouda.

1. Article 3, para 1, REGULATION (EU) 2022/2560

2. Article 4, para 1, Article 3, REGULATION (EU) 2022/720

![tracking-pixel]()