Cyber security threats are constantly evolving. We’ll work with you to develop and test robust people, process and technology defences to protect your data and information assets.

Working with borrowers and private equity financial sponsors on raising and refinancing debt. We can help you find the right lender and type of debt products.

Regulatory change, pressure on cost management and growth, and increased investment in technology and data are dominating the financial services industry.

Looking for a more fulfilling role in professional services? One where fresh thinking, collaboration and diversity are valued? At Grant Thornton we do things...

Included and valued for your difference is how everyone should feel at work. Not just because it’s right, but because we’re all at our best when we’re able to be ourselves.

Our ESG framework enables responsible, sustainable, and ethical operations. We prioritise the environment, our broader societal impact, and our firm's governance to protect the planet, foster inclusivity and wellbeing, support our communities, and bolster our firm's resilience.

Our employability hub is designed to help you feel prepared for the application process, and guide you through the decisions you will need to make throughout.

Whether you are looking to join us straight from school or with a degree, or even looking for some work experience, we have a programme that is right for you.

We hope you can find all the information you need on our website, but to help we've collated a few of the questions we hear quite frequently when speaking to candidates.

Looking for a more fulfilling role in professional services? One where fresh thinking, collaboration and diversity are valued? At Grant Thornton we do things...

Our advisory practice provides organisations with the advice and solutions they need to unlock sustainable growth and navigate complex risks and challenges.

We strive to ensure our interview process is barrier free and sets you up for success, as well as being wholly inclusive and robust. Learn about our process here.

As an Armed Forces Friendly organisation we are proud to support members of the Armed Forces Community as they develop their career outside of the Armed Forces.

Are you a partner or director, or on track to one of these positions? Are you looking for a more exciting role where you can drive change and help shape the...

The Agile Talent Community is a network of contract professionals given the opportunity to work with valued clients on a project-by-project basis and provided...

Financial pressures remain a huge challenge for the NHS in England and financial sustainability is at a critical point. Peter Saunders, Emily Mayne, and Nick Caley share some clear actions Trusts can take to regain control.

Contents

Having emerged from the worst of the COVID-19 pandemic, NHS finances have come under sustained pressure as the service deals with multiple challenges, including rising waiting lists, high inflation, workforce gaps, industrial action, and a creaking infrastructure. Our analysis earlier in the year identified the underlying drivers of financial performance in 2022/23 and these were flagged as clear risks to delivery during the 2023/24 planning process.

Key insights from NHS audits

Our audits of the 2022/23 NHS accounts include judgements on financial sustainability and governance, as part of the responsibility to assess Value for Money (VfM) arrangements outlined by the Audit Code of Practice. We've used information from the Auditor’s Annual Report (AAR) for 58 NHS trusts where Grant Thornton is the external auditor to highlight the principle challenges for NHS finances.

Financial performance of NHS Trusts is significantly deteriorating

Deficits doubled in value when comparing 2022/23 actuals to 2023/24 plans, with financial distress particularly evident across the acute sector. This is on the back of short-term, non-recurrent measures propping up the 2022/23 position of many Trusts.

41% of NHS Trusts have significant weaknesses in financial sustainability and governance

This is a material increase compared with 2021/22 (10%) – auditor assessments were worse at our NHS trust acute audited bodies where 63% had significant weaknesses identified. The main causes of these assessments were the lack of detailed Cost Improvement Plans (CIPs) for 2023/24 and the existence and maturity of medium term financial plans.

The CIP target included in 2023/24 plans was 65% higher than that delivered in 2022/23. Plans showed this increase would be delivered wholly from recurrent savings. The average CIP target was 5% of income, but there was a range from 2.7% to 9.1% across the 58 Trusts.

Many Trusts had under-developed recurrent and medium-to-long term programmes to bridge planning gaps in their finances. Almost half of savings delivered in 2022/23 were non-recurrent, one-off cost reductions, such as centrally held non-recurrent funding, unspent reserves, and balance sheet adjustments. The majority of Trusts we audited had underlying, operational deficits (up to £150 million in our sample) but no agreed plans with system partners for medium term financial sustainability.

VfM work includes the consideration of the arrangements in place at NHS organisations to ensure proper governance, resource and risk management, and internal controls, and are reported under three specified criteria:

Financial sustainability

How the Trust plans and manages its resources to ensure it can continue to deliver its services

Governance

How the NHS Trust ensures that it makes informed decisions and properly manages its risks

Improving economy, efficiency, and effectiveness

How the NHS Trust uses information about its costs and performance to improve the way it manages and delivers its services

The financial sustainability criteria within the VfM framework requires auditors to assess how Trusts plan to bridge funding gaps and identify achievable savings and support the sustainable delivery of services in accordance with strategic and statutory priorities. It also covers how the Trust

identifies all the significant financial pressures that are relevant to its short and medium-term plans and builds these into them

ensures its financial plan is consistent with other plans, such as workforce, capital, investment, and other operational planning, which may include working with other local public bodies as part of a wider system

identifies and manages risks to financial resilience

Financial performance

The financial performances of Trusts are deteriorating significantly. From the sample of audited bodies analysed, planned deficits (agreed with NHS England) in 2023/24 total £521 million compared to actual reported deficits of £249 million in 2022/23 – a doubling of deficits in one year.

The underlying position is considerably worse. It's widely reported that financial plans in 2023/24 are challenging and that Trusts and auditors have identified significant risks with their delivery. The use of short-term, non-recurrent measures also propped up the 2022/23 position of many Trusts. The most recent financial report from NHS England already identified overspending of £809 million at month four (July) against these plans.

Our analysis shows continuing widespread financial pressure on the NHS acute sector, with community, and mental health Trusts performing better.

Source: VFM audit findings as reported in the Grant Thornton 2022/23 Annual Audit Report for 58 Trusts, comprising 35 acute, 11 mental health, 6 community, and 6 specialist Trusts.

Financial sustainability

For 2022/23, ourauditorshave materially increased the number of significant weakness judgements for financial sustainability, compared with 2021/22. 41% of our Trust audited bodies had financial sustainability significant weaknesses reported - a significant increase from the previous year (10%). Approximately 63% of our acute trust audited bodies received significant weakness judgements – reemphasising that this is a key sector of financial distress.

Summary of financial sustainability findings from VfM audits

Source: VFM audit findings as reported in the Grant Thornton 2022/23 Annual Audit Report for 58 Trusts

In total, auditors made 119 recommendations to improve financial sustainability and financial governance across the 58 NHS trust audited bodies. More than two thirds of Trusts have recommendations relating to 2023/24 Cost Improvement Plans (CIP) and delivery, and the development of longer-term financial plans. Auditors also identified improvements to financial reporting around the quality of reporting of system financial performance to boards, use of costing information, improvements to monthly finance reports, and clarity of reporting of assumptions, risks and scenarios. They also highlighted the use of short-term financial fixes, such as one-off non-recurrent schemes and technical, balance sheet adjustments, and reviews to underpin financial performance.

Source: VFM audit recommendations, both key and improvement, as reported in Grant Thornton 2022/23 Auditor's Annual Reports for 58 Trusts

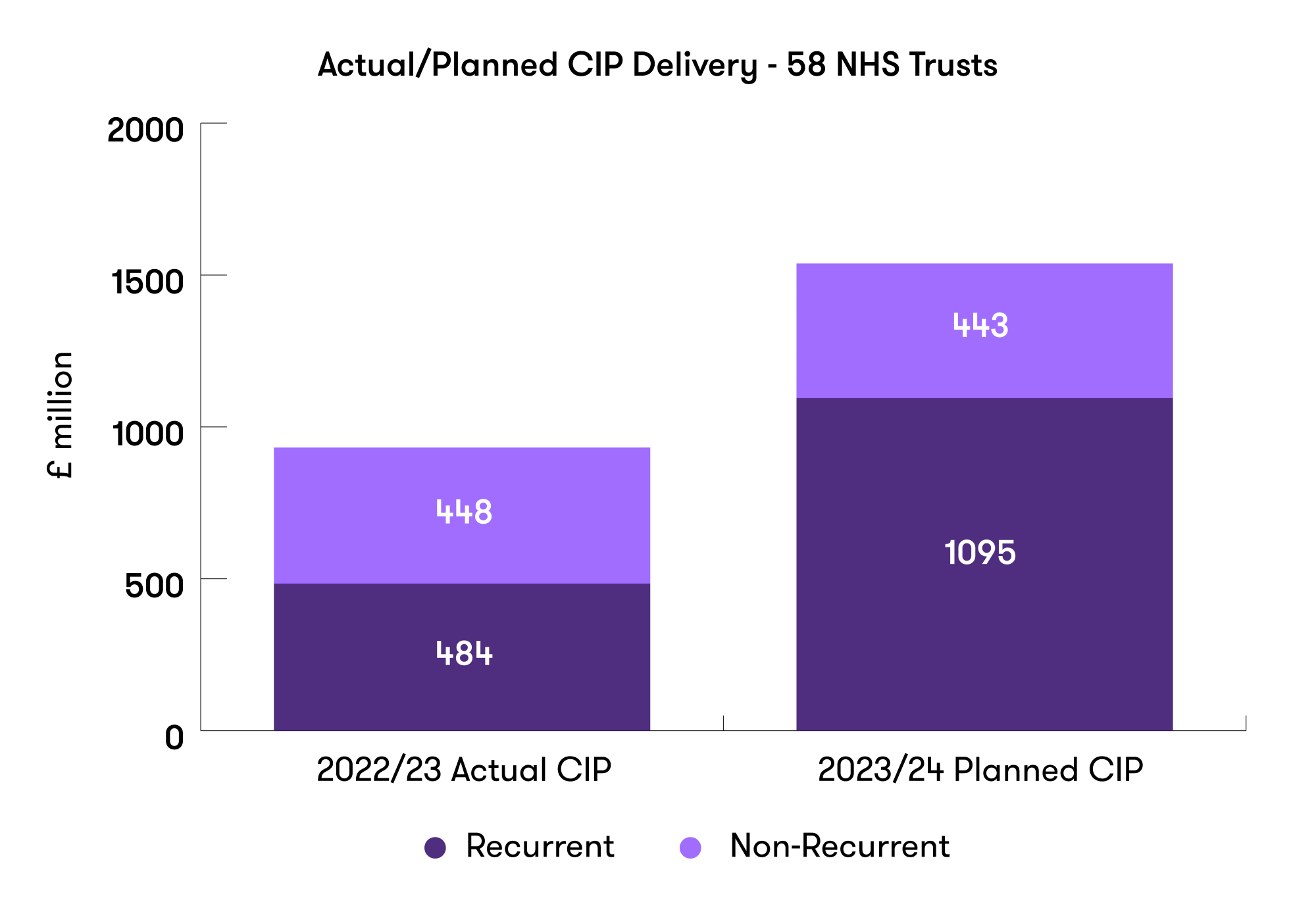

Cost improvement planning and delivery

Across 58 Trusts, the CIP target included in 2023/24 plans is £607 million higher (65%) at £1.5 billion compared with £932 million delivered in 2022/23. Plans showed this increase would be delivered wholly from recurrent savings. On average, the CIP challenge in 2023/24 equates to 5% of income, with this ranging from 2.7% to 9.1% across the 58 Trusts. This very large increase in CIP in 2023/24 is happening at a time of continuing operational difficulties with urgent and emergency care, as well as cost-of-living and workforce challenges.

Source: VFM audit findings as reported in the Grant Thornton 2022/23 Auditor's Annual Report for 58 Trusts

During 2022/23 Trusts returned their focus to operational productivity, with workforce growth compared against pre-pandemic levels being a key area of focus.

Many Trusts had under-developed recurrent and medium to long-term programmes to bridge planning gaps in their finances. They also had ineffective monitoring arrangements for tracking the financial impact of operational productivity improvements at a Trust and system level. Trust schemes are still generally aspirational, temporary, and non-recurrent. There's also limited evidence of system-wide productivity measures delivering significant benefits. Much more work still needs to be done to deliver significant cost and waste savings through system collaboration to build financially sustainable plans.

Almost half of savings delivered in 2022/23 were non-recurrent, with examples of one-off cost savings including centrally held non-recurrent funding and unspent reserves - largely as a result of the COVID-19 funding regime: VAT reviews, releasing provisions and other balance sheet adjustments. These short-term, non-recurrent measures were a key area of focus for audit testing and don't contribute to creating longer term financial sustainability.

There are steps you can take now to recover, transform and innovate to create a sustainable, quality-driven NHS for the future.

The majority of Trusts we audited had underlying, operational deficits (up to £150 million in our sample) and no agreed plans with system partners for medium term financial sustainability. Non-recurrent funding and adjustments continue to obscure the underlying operational financial position of many hospitals. Understanding the true financial baseline and drivers of performance is the starting point for financial sustainability.

Detailedthree to fiveyear financial plans can help demonstrate the scale of financial turnaround required and set the stage for clinical, workforce, and operational plans and strategies. This shouldn’t be something that's only produced for regulators – it’s a fundamental component of service management and planning.

Reviewing long term operational and financial plans (including long term CIP programmes) – and regularly updating them needs to become business as usual and not just part of the annual planning process. This will help to broaden the understanding of the risks and challenges with clinical and operational leadership as well as regulators. Financial plans need to be underpinned by models showing the impact of service changes, investments and transformation, and productivity programmes with scenario planning. To be credible it's vital that there's genuine triangulation of operational performance and activity, workforce, quality impact, and finances.

Delivering financial sustainability

Financial plans for 2023/24 included stretching targets and optimistic assumptions, with most Trusts reflecting significant risks to delivery. Already we're starting to see clear warning signs that Trusts and systems are struggling to hit year-to-date targets and the re-emergence and appointment of turnaround directors in systems which are financially challenged. Our analysis does suggest several actions that successful NHS Trusts will take.

Getting back to basics

Ensuring key information and data is updated and accurate so there's a clear understanding to build reliable analysis on, including demand and capacity modelling, costing, service line reporting, data and coding accuracy, and workforce information and analysis.

Understanding the real operational financial position

Stripping out non-recurrent income and costs and ensuring workforce is the right size for agreed activity plans and productivity plans. Evaluating contribution and service level financial performance.

Maintaining and restoring financial control and process

Ensuring the whole organisation manages its overall spending effectively by reinforcing the need for strong financial control.

Investing in developing and delivering multi-year, recurrent cost improvement programmes

Both Trusts and wider systems need to work together to deliverthree to fiveyear plans by providing capacity and joining up work to develop long term opportunities to balance the books. Establishing effective management and monitoring arrangements to ensure these are tracked and provide assurance over their delivery.

Effective engagement and ownership with clinical and operational teams

Working with clinical and operational leaders to provide an understanding of the overall financial picture, spending issues and patterns, and supporting the need for efficiency and delivering programmes.

Developing a medium-term financial plan

In our experience few Trusts have a clear and detailed medium term financial plan over the medium/long term. The need to develop this working alongside system partners is a key requirement to build and restore confidence in Trust plans and deliver financial sustainability. A medium/long-term financial model can also be a useful tool to shift focus on to the challenges beyond the current year and can really help Directors of Finance to quickly show the multi-year impact of different assumptions and scenarios.

Within discussions of NHS crises, the financial position is not being fully considered. We explore why and what to do.

All of these actions have to be balanced against the need to deliver safe patient care, timely access to services, and the sustained day-to-day operational pressures that the NHS faces. It's no wonder NHS leaders are scratching their heads on how this all can be achieved. And as challenging as it is, transparency and understanding ofthefinancial position are critical in interactions with boards, regulators, and auditors.

Source: VFM audit findings as reported in the Grant Thornton 2022/23 Annual Audit Report for 58 Trusts

Source: VFM audit findings as reported in the Grant Thornton 2022/23 Annual Audit Report for 58 Trusts